What is Trade Credit? Here are the Advantages and Disadvantages

Trade credit is a form of short-term B2B financing that can free up working capital and finance growth.

July 14, 2025

-

0

min read

Trade credit is a form of short-term B2B financing that can free up working capital and finance growth.

0

min read

If your business is heavily reliant on suppliers of goods or materials, managing cash flow can be a tricky balancing act. Trade credit lets you pay your suppliers later down the line, to ensure you’ve got a healthy working capital for operations while waiting for revenue from customer sales or client invoices.

But what is trade credit, and how does it work? In this article, we break it down, discussing the advantages, disadvantages and how to leverage this crucial form of B2B financing.

Trade credit is a short-term form of business finance that not only helps companies ease cash flow concerns but also strengthens ongoing business-supplier relationships. Put simply, the concept involves one business agreeing with another to supply something now and letting the other business pay for the goods later.

Around 80-90% of world trade relies on trade credit financing of some kind, according to the World Trade Organization. It’s mutually-beneficial two-way business transaction between the supplier and buyer.

Terms are usually agreed upon upfront, often simply by one company deciding to do business with another. Usually, the supplier gives the buyer between 30, 60 or 90 days to pay.

However, you can use intermediaries that support the financing agreement (usually with BNPL technology), making the process more efficient, enabling more flexibility and reducing risks. In this case, the third-party provider charges a percentage on transactions (typically 2-8%). For the buyer, the solution enables interest-free payments up to a certain number of months, and sometimes a flat monthly fee.

By receiving the goods or materials you need without a large initial outlay, you can use or sell them to bring money into your business to keep operations moving and support growth, before paying the supplier when you have the cash.

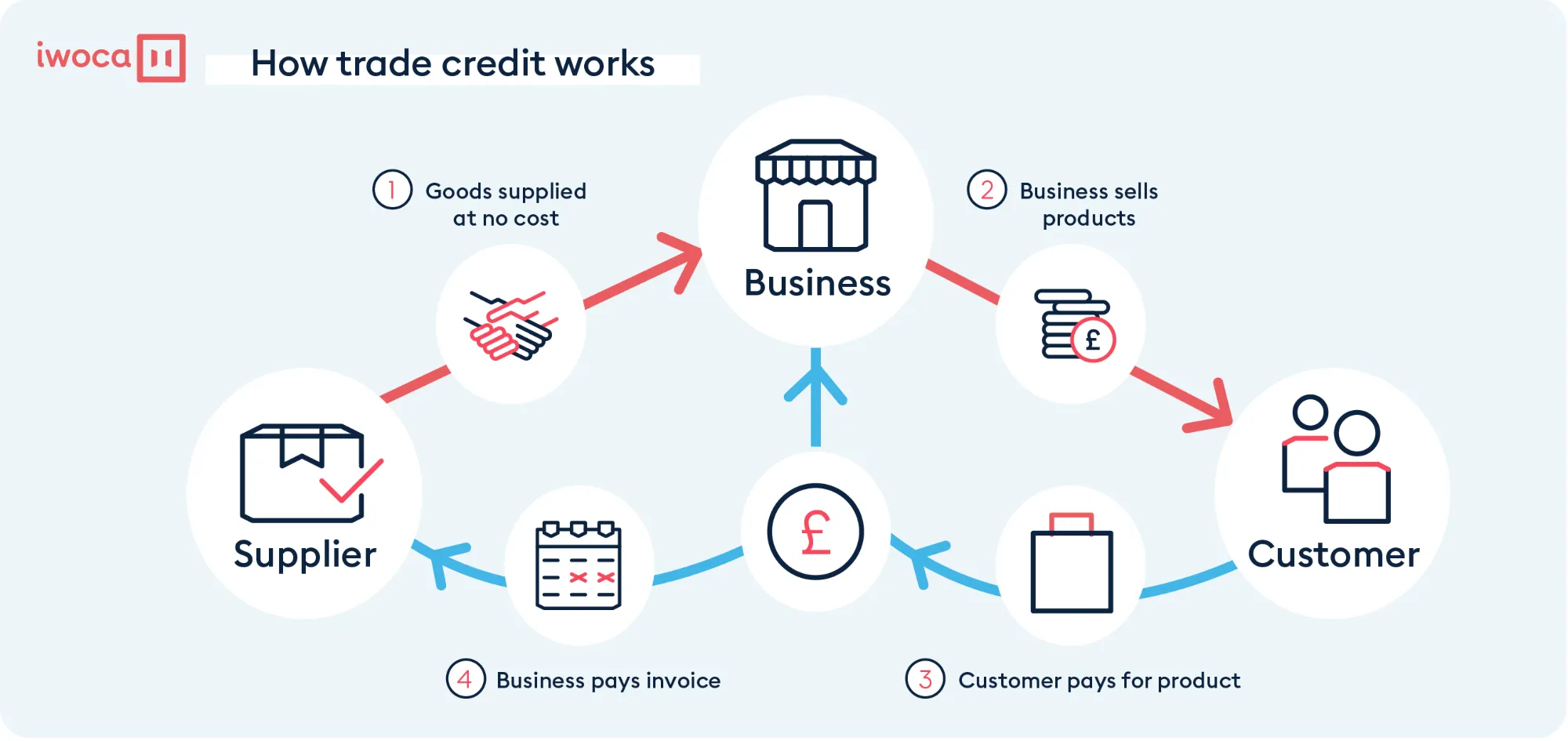

Here’s a graphic to give you a visual look at the flow of how trade credit works:

Trade credit is the bedrock of business and the greatest facilitator of global and local trade from supermarket shelves to shipyards and construction sites. In financial terms, trade credit is a form of deferred payment. In business terms, it's the foundation of a mutually profitable relationship.

While the fundamental concept of trade credit is clear, businesses have various uses for trade credit, such as:

If you're on the receiving end, it's like having a short-term, unsecured, interest-free loan to buy the goods and materials you need. This puts assets in your hands that your business can use to generate income, with no drain on your working capital and a lot less pressure on your cash flow.

Some businesses simply couldn't exist without trade credit. Imagine having to pay for everything right away, all that cash tied up until the money comes in from your customers.

Here are some examples of businesses that are heavily reliant on the use of trade credit:

Unless you have huge cash reserves or significant profit margins, you need this credit buffer to manage working capital effectively.

There are nuances involved, though, and terms can be negotiable. Most suppliers incentivise early payment to help their own cash flow. For example, a supplier might give you 90 days to pay, but offer a discounted rate if you pay within, say, 14 days. Alternatively, buyers influenced by seasonality can ask suppliers for a temporary increase in credit limit or payment timeline to accommodate fluctuating demand.

What are the main advantages and disadvantages of trade credit?

As with any financial agreement, trade credit has both advantages and disadvantages, and these differ for buyers and suppliers. Trade credit can fuel growth, increase turnover, add a competitive edge and boost loyalty, but it can also expose suppliers to cash flow problems.

The advantages outweigh the disadvantages, but it’s important to understand the risks of the financing agreements. Below, we outline the main pros and cons to consider.

While traditional trade credit and BNPL (buy now, pay later) for B2B are similar, they’re structured and executed differently. Standard trade credit involves direct terms with sellers, who assess buyer creditworthiness, consider the risks and handle payment collections, which can prove time-consuming. In contrast, B2B BNPL involves a third-party provider handling credit checks, approvals and repayments, using advanced credit tools that integrate easily with sales platforms and simplify payment processes.

These B2B BNPL providers assume the financial risk, paying the seller upfront while managing buyer repayments. For SMEs, it lowers the barrier to accessing credit. It shares similarities with invoice trading and invoice financing, in that it supports cash flow management and prevents upfront costs or delayed payments from limiting available working capital.

Explore our guide to BNPL and trade credit solutions to understand which might be best for your business.

Like any financial arrangement, using credit comes with a degree of risk, one of them being the potential impact on your credit rating. But responsible use of trade credit and prompt repayments (within agreed deferred payment timelines) will help maintain and build your business credit score. Adversely, misuse and late payments will negatively impact your rating, making it harder to borrow capital in the future.

If you’re a sole trader, a new business, or you’re required to provide a personal guarantee, your personal and business credit scores can be affected, as the lines between your finances become blurred. Also, some lenders will check both credit files during vetting and approvals.

In some cases debt default can cripple a business. Sadly, insolvency, where a business cannot pay its debts, is not uncommon. Trade credit insurance is designed to protect a supplier against excessive late payments or non-payment for goods or services supplied on credit. A credit insurance policy gives suppliers peace of mind that a company’s potential cash flow problems won’t have serious consequences for their own business.

The insurance also helps safeguard companies from wider risks, such as fluctuations in international trade or government intervention in a particular business sector.

Various UK providers enable B2B BNPL solutions for businesses. We’ve outlined some of the best BNPL trade credit providers in the table below, including our own solution, iwocaPay, along with some key information about each provider:

iwocaPay is a fast, simple and flexible BNPL trade credit solution designed for the needs of UK SMEs. It integrates with top ecommerce and accounting software, such as WooCommerce, Shopify, Magento 2, QuickBooks and Xero, to deliver a seamless credit solution for both sides of the trade relationship.

If you’re a supplier, iwocaPay provides a hassle-free way to offer your customers trade credit while you receive instant advanced payments, which has helped our suppliers increase average order value by 45%.

For businesses that need to purchase goods or materials from suppliers without a big upfront outlay, you can spread the cost and choose from a range of Pay Later options, with a spending limit of up to £30,000. We’ll conduct a soft credit check before accepting you into our trade credit solution, meaning it won't affect your credit score.

Check out how iwocaPay works and see how our solutions could ease your cash flow challenges and simplify supplier payments.

If you’d like more information on the topic, we have a collection of handy trade credit resources to help you. Here are some relevant articles to explore:

iwoca is one of Europe's leading non-bank lenders. Since 2012, we've lent over £4.5 billion to 100,000 small and medium-sized businesses in the UK and Germany.

iwoca has won a number of awards, including Moneynet's best small business lender (2024) and best small business provider (2025). We've also been featured in major media outlets including The Independent, Forbes and the Financial Times.

With iwoca, draw down as needed and repay early to save on interest. Flexible business loans with no hidden fees.

Trade credit is a form of short-term B2B financing that can free up working capital and finance growth.