Unsecured business loans explained

Borrow £1,000 to £1 million without putting up your business assets as collateral. We do ask a company director for a personal guarantee - here's exactly what that means.

- No business assets as collateral

- Borrow £1,000 to £1 million over one day to five years

- No fees for repaying early

What is an unsecured business loan?

An unsecured business loan lets you borrow without securing the loan against the business's property, equipment or other assets. If you can't repay, the lender can't automatically take those assets.

That makes unsecured loans quicker to arrange and open to businesses that don't own big assets. In return, lenders usually ask a director for a personal guarantee – more on that below.

At iwoca, we've made the decision to only offer unsecured business loans – so your business assets stay yours.

Secured vs unsecured: which is right for you?

a secured loan may cost less.

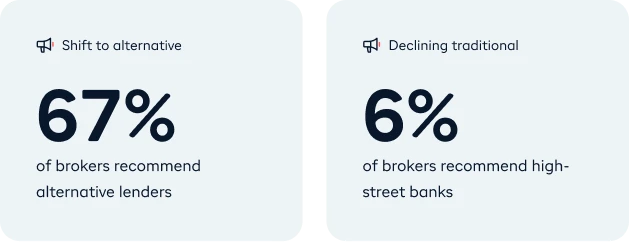

Brokers are turning away from the banks for bigger loans

When a small business needs to borrow over £100,000, most finance brokers now point them to alternative lenders like us, not the high street.

What a personal guarantee means

Because our loans are unsecured, we ask a company director to give a personal guarantee. This is a commitment to take personal responsibility for the loan if the business can't repay it.

In plain terms: if you: if your business can't repay and can't agree a way forward with us, you as the guarantor would be responsible for the outstanding balance. It's worth understanding this fully before you apply.

It's a serious commitment, so we're upfront about it. A personal guarantee lets us lend larger amounts at better rates than we could without one – because it lowers our risk. And we only lend to businesses we're confident can pay us back, so it rarely comes to this.

If you ever think a repayment might be tricky, just talk to us early and we'll work out a way forward together.

Who can get an unsecured business loan?

A limited company or limited liability partnership

Based in the UK

You are at least 18 years old

Advantages and disadvantages of an unsecured loan

- No need to tie up business assets

- Faster to arrange than a secured loan

- Open to businesses without big assets

- Draw down what you need, repay early with no fees

- Usually needs a personal guarantee from a director

- Terms tend to be shorter than secured loans

- Rates reflect that there's no collateral

- Missed payments can affect your credit file

Unsecured loan FAQs

What is an unsecured business loan?

It's a loan that isn't secured against the business's assets. If you can't repay, the lender can't automatically claim your property or equipment. Instead, lenders usually ask a director for a personal guarantee.

Secured or unsecured – which should I choose?

Unsecured suits businesses that want funding quickly without tying up assets. Secured can cost less for very large amounts over many years, but takes longer to arrange and puts an asset on the line.

Do unsecured loans need a personal guarantee?

With iwoca, yes – we ask a company director to give a personal guarantee. It means taking personal responsibility for the loan if the business can't repay. It lets us lend more, at better rates, than we could otherwise.

What happens if I can't repay?

Talk to us as early as you can and we'll try to work out a solution together. If a loan isn't repaid and we can't agree a way forward, we may ask the guarantor to cover the balance, and missed payments can affect their business credit file.

Can a new business or startup get one?

Yes. We look at how your business is performing rather than only your trading history. If you've been trading under a year, loans are capped at £10,000.

What do I need to apply?

A few details about your business and your recent bank statements. For larger loans we might ask for VAT returns or full accounts. You won't need a business plan or forecasts. Applying won't affect your credit score.

%20(1).jpg)