Invoice finance helps businesses to improve cash flow, pay both suppliers and employees, and invest in growing your business faster than if you had to wait on your customers paying their outstanding invoices.

Invoice finance is a short term funding option that allows you to benefit from the value of outstanding invoices by receiving a percentage of their value in advance of their payment date. It’s like being paid early, or on time if the customer is late, at the cost of a percentage of that value. The amount you are charged for this service varies based on the profile of the customer you are invoicing and how much you intend to borrow, but could be as low as 10%.

Note, this type of finance is generally only suitable for businesses that invoice larger companies for goods or services. Also you may be responsible for repaying the full value of the invoice if your customer fails to pay.

How does invoice financing work?

Invoice financing operates as a means for businesses to unlock cash tied up in unpaid invoices.

Businesses sell their outstanding invoices to a finance company, also referred to as a factor.

The factor typically pays the business around 85% of the invoice value upfront.

Once the invoice is fully paid by the debtor, the business receives the remaining balance, minus the factor's fees.

This practice aids in maintaining a healthy cash flow, especially in instances where customers may take a long time to pay their invoices. It's a common practice among small to medium enterprises (SMEs) that operate with longer payment terms.

Invoice financing calculations

While the terms can vary from lender to lender, it can be useful to look at an example of invoice financing to see how it works.

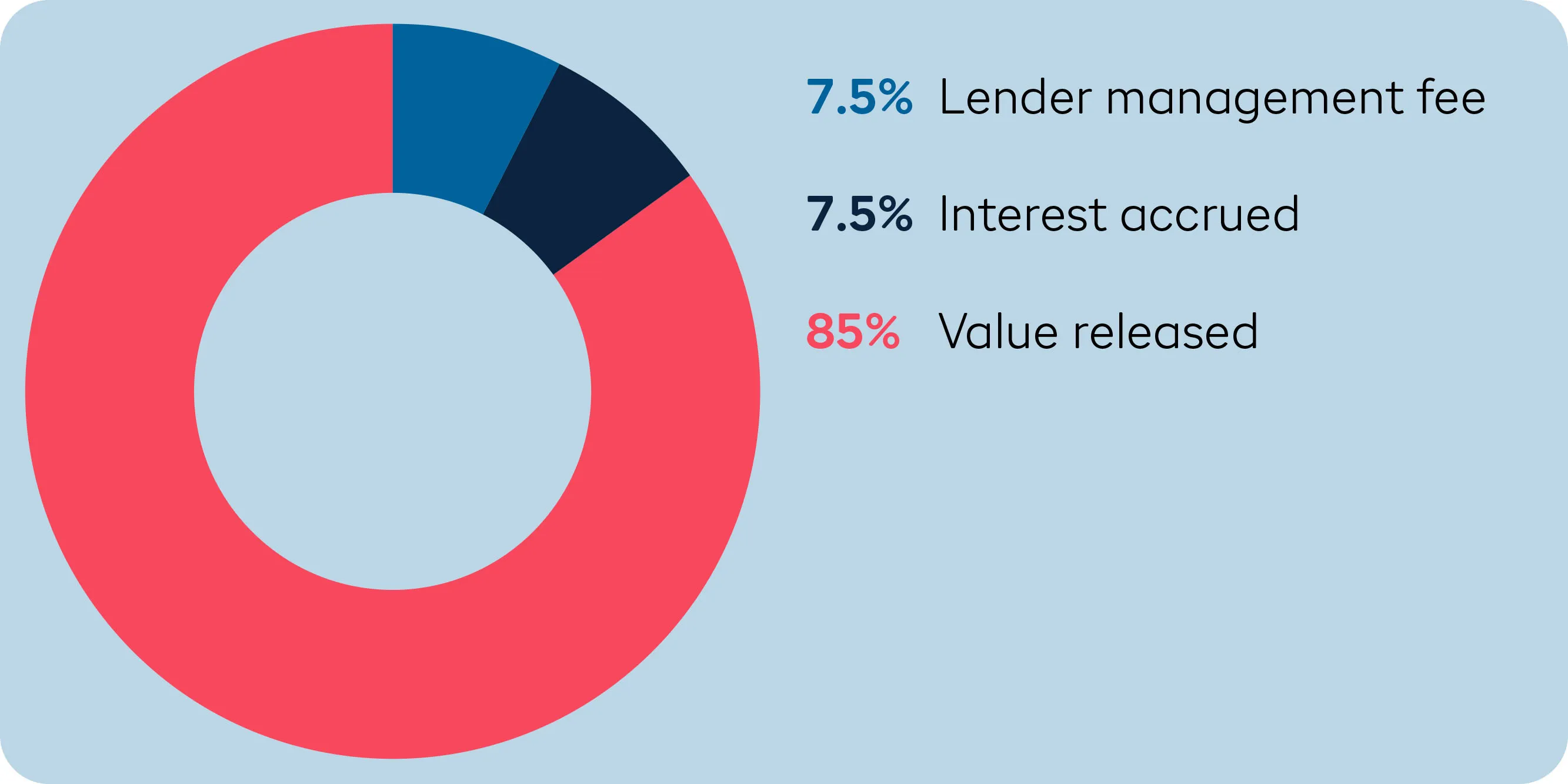

Costs for invoice financing come both from the fee from the lender as well as the interest on the sum borrowed.

In this example, the business is able to unlock 85% of the outstanding invoices value, paying 7.5% in fees and 7.5% in interest.

Example of invoice financing

A graphic design company has completed a lot of work, but is waiting on unpaid invoices from their customers

The owner is short on working capital, so they take 10 outstanding invoices totalling £50,000 and factors them for 85% of their value

They receive the £42,500 advance from an invoice finance provider

The finance provider then chases the design company’s customers for the value of the invoice

The customers pay the finance provider, who collates the funds

The designer then receives the remaining value of the invoice minus interest and a management fee.

{{flexi-loan="/components"}}

What are the advantages and disadvantages of invoice financing?

Invoice financing is just one kind of small business finance option, and it comes with its own considerations. Check out the list below to understand whether it’s right for you.

Advantages of Invoice Financing

Faster access to cash: One of the primary benefits of invoice financing is the immediate boost to cash flow. Businesses can access up to 90% of the invoice value almost immediately, which helps manage day-to-day operations without waiting for customer payments.

Short term flexibility: Unlike traditional loans, which may require a long-term commitment, invoice financing offers flexibility. Businesses can choose which invoices to finance and when

Ease of approval: Since the financing is secured by the invoices themselves, businesses with less-than-perfect credit can still obtain funding. This makes it easier for newer and smaller businesses to access the capital they need without the steep requirements of traditional bank loans.

Simplicity: For options like invoice factoring, the lender often takes over the management of the sales ledger and collection process.

It’s not debt: Since it's not considered a loan, invoice financing doesn't add to a company's debt levels, keeping the balance sheet clean and more attractive to potential investors or lenders.

Disadvantages of Invoice Financing

Higher costs: Invoice financing can be more expensive than traditional loans due to higher fees and interest rates. It’s important to consider the cost-effectiveness of the service, weighing the fees against the immediate benefits of improved cash flow.

It’s not a fix: Relying heavily on invoice financing can lead some businesses into a cycle of dependency, where they are continually financing invoices to cover short-term cash needs, potentially hiding underlying financial problems.

Giving up customer interactions: In the case of invoice factoring, customers deal directly with the factoring company to settle their invoices. This can impact the customer-business relationship, especially if the factoring company does not handle collections in the same way you would.

It’s not right for all businesses: Invoice financing is typically only suitable for businesses that invoice other businesses (B2B).

What are the different kinds of invoice financing?

There are a range of ways you can use your invoices to generate capital, with different costs, timelines and responsibilities involved. Below you’ll find the key types of invoice financing you need to know:

Recourse financing?

With recourse financing, your organisation agrees to take full liability for the invoice you've borrowed against. That means if it's unpaid by your customer then you'll be required to repay the money you have been advanced in full.

The remaining value of the invoice (usually between 10% and 30%) is held in reserve by the lender until your customer has made the full payment. The interest and management fee charged by your provider are deducted from this, and the rest is transferred to you. Those fees can vary hugely depending on which provider you choose.

Non-recourse financing

With non-recourse financing, if your customer fails to pay their debt, your invoice finance provider will be liable for the losses incurred.

This is sometimes subject to limitations, so be sure to read the small print carefully. Because invoice financing on a non-recourse basis is riskier to the lender, it's often more expensive and much more difficult to get approved for than on a recourse basis.

Selective invoice finance

Selective invoice finance, often known as spot factoring, is a flexible type of invoice financing used in the UK. Unlike whole ledger invoice finance, where you are obligated to factor all your invoices, selective invoice finance allows you to choose specific invoices to factor.

This means you can decide to finance only high-value invoices or those from customers with long payment terms to maintain cash flow. It's quite an beneficial option for you if you don’t want to commit to long-term contracts or if your business is seasonal. This method provides immediate funds and can be a cost-effective alternative, given that fees are only applied to the selected invoices.

What’s the difference between invoice financing vs discounting

Invoice financing actually refers to two related, but slightly different, financial services – invoice discounting and invoice factoring. Both allow you to use your invoices as collateral to secure a credit line, but their differences are important.

Invoice factoring

Invoice factoring, also known as debt factoring, is a contract involving an invoice finance provider managing your sales ledger and collecting money owed by your customers themselves.

This means your customer will be fully aware you’re using invoice finance. Using invoice factoring can free you from time-consuming invoice collection and allow you to concentrate on your business. Most invoice finance providers want you to have a sales volume of more than £250,000 per year before they’ll consider factoring your invoices.

Invoice discounting

Invoice discounting is different from factoring in that your customer’s payments are directed to a trust account in your name, held by your invoice finance provider. This means your provider won’t take responsibility for collecting payment for the invoice, so your customer won’t know that you’re using invoice finance.

It is usually only available to companies which turn over more than £1 million per year. Invoice discounting permits you to maintain close ties to your customers and continue to manage your sales ledger yourself. You might prefer this if you’re worried about how your finance provider might manage the collection of your invoices.

What are the costs of invoice financing

Typically, there are two main costs associated with invoice financing

The amount of interest you'll pay for advancing your invoices

The invoice finance rates you'll pay on top of this

Interest rates for this type of funding are similar to invoice factoring and invoice discounting, and are usually between 1.5 and 3% per year above the Bank of England base rate. Management fees are paid on the total value of the invoices you advance. This is generally around 0.2% - 0.5% with discounting, and 0.75% - 2.5% with factoring.

This means invoice factoring is much more expensive than discounting. This is because the factoring provider has taken over responsibility for chasing your invoices for repayment, and takes on the extra cost of this service. You should also be wary of any additional fees the invoice finance provider might charge (see their FAQs for details).

Besides interest and management fees, are there other costs to consider?

There are a range of invoice finance rates that you might be charged when using invoice financing. Here’s a run-down of the fees you should consider:

Set up fees: a fee that is typically charged for setting up the facility.

Survey fees: some lenders may want to survey your business as part of their due diligence. Some lenders offer this free of charge while others charge a fee for it.

Audit fees: lenders could require an audit of your business. It is important you understand the charges and what frequency they will take place.

Re-factoring fees: some lenders will charge a fee on invoices that are outstanding after a certain number of days.

When you factor or discount your invoices, you're using their value as collateral for the advance payment. This means you usually won't have to sign a personal guarantee.

Other options for small business financing

If you’re in need of short term financing for your business, iwoca can help you connect to capital fast. You can apply for a flexible business loan in minutes, with decisions based on your actual business performance. Once approved, the funds can be in your account in hours.

iwoca is one of Europe's leading non-bank lenders. Since 2012, we've lent over £4.5 billion to 100,000 small and medium-sized businesses in the UK and Germany.

iwoca has won a number of awards, including Moneynet's best small business lender (2024) and best small business provider (2025). We've also been featured in major media outlets including The Independent, Forbes and the Financial Times.

Start accepting payments with iwocaPay

Trade customers split payments into 1,3 or 12 monthly instalments

Online and in store, on orders up to £30k

You get the funds instantly, every time, with no recourse

Invoice finance helps businesses to improve cash flow, pay both suppliers and employees, and invest in growing your business faster than if you had to wait on your customers paying their outstanding invoices.