Join over 100,000 businesses growing with iwoca

Reward your spending and smooth your cashflow

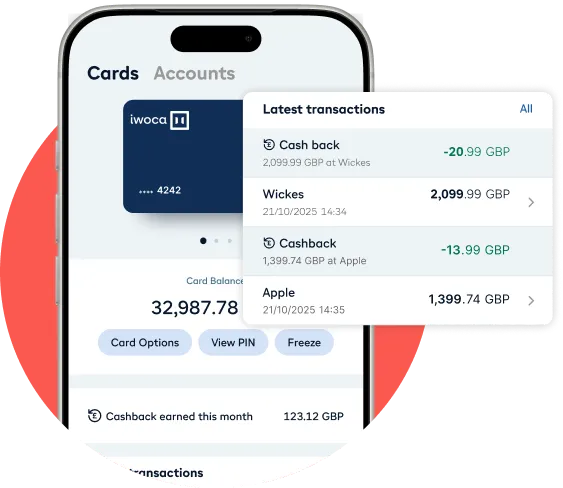

1% cashback

on all spending

Get rewarded instantly with cashback that’s automatically applied to your balance.

Easy-to-use

app

Stay in control with real time spending information.

No interest for

up to 42 days

Smooth cashflow and pay no interest when you repay in full and on time.

Interest rates start at 14.99% per year, with representative 35.40% APR (variable).

Why chose the iwoca Credit Card

Stay in control

Our simple app makes it easy to keep track of your spending and repayments.

Smooth cashflow

Bridge gaps or cover unexpected costs and pay no interest when you repay in full.

Reward your spending

1% cashback is automatically applied to your account for every payment.

Boost your credit score

Use your card and make repayments to build your credit history and access other finance.

Simplify bookkeeping

Separating personal and business expenses makes tax preparation easier.

How to apply

Apply online in 5 minutes

No long forms or drawn-out questionnaires, we’ll just need some basic information about your business.

Get a decision instantly

Keep your momentum going with real-time decisions that don’t affect your personal credit score.

Start spending straight away

Once your account is created, just download the app and start spending.

Already signed up?

Download the app now

What is a business credit card?

A business credit card is a powerful financial tool for companies. It functions like a personal card but is used to manage cashflow, track spending, and build a business credit history while offering rewards or benefits.

Frequently asked questions

Here are a few of our FAQs. Can’t find what you’re after? Try our longer list.

The iwoca Credit Card offers you up to £250,000 credit with no fees. You’ll earn 1% cashback on all card spend. Your cashback will be automatically added to your account and reduce your outstanding balance.

You’ll also have up to 42-days interest free which means if you repay your balance in full every month, you’ll pay no interest.

Your business credit card is used for business spending and can help build your business credit, while a personal credit card is used for your personal spending.

Separating your business spending onto a different card makes financial tracking and tax preparation a lot easier and can save you time.

To be eligible for the iwoca Credit Card, your business needs to:

- Be based in the UK

- Be a limited company or a partnership

It’s free to apply and it won’t affect your personal credit score.

Yes, most businesses, including iwoca, require a personal guarantee. This means that if the business is unable to afford monthly repayments, the guarantor becomes personally responsible for repaying any outstanding balance.

Business credit card APRs vary based on the card issuer and your creditworthiness. While often higher than personal rates, you can avoid interest charges if you pay your balance in full each month. This also helps build a strong business credit score and can improve your future borrowing power.

The Interest rates for an iwoca Credit Card start at 14.99% per year, with representative 35.40% APR (variable). Find out more about how APR is calculated here.

When your statement is ready, you will need to pay at least 10% of the outstanding balance or £100, whichever is higher. You can also choose to pay off more or repay your whole balance. You can change your repayment preferences at any time by logging into your account. It’s important to note that if your outstanding balance is less than £100, you will need to repay in full.

At the end of each monthly billing period, we'll send you a statement. It'll show all your transactions, the cashback you’ve earned, your total balance and the minimum repayment due.

You'll then have 12 days once your statement has been generated to make a repayment. You must set up a direct debit so that your repayment can be taken automatically on the given date.

This tells you the maximum amount of time between a purchase and your payment due date. For an iwoca Credit Card, the 42 days is made up of your 30 day billing cycle plus a 12 day grace period before your payment is due. For example, let’s say you buy something on day one of your cycle, you get the full 42 days of interest-free credit. If you make another purchase on day 30, you get 12 days on that purchase.

To avoid paying interest, you must pay your statement balance in full by the due date each month.

Yes, you can use your iwoca Credit Card abroad and still get 1% cashback on your transactions. We don’t charge you any foreign exchange (FX) fees, which means we pass on Visa’s rate straight to you.

Unfortunately, you are not able to withdraw cash using your iwoca Credit Card, but we hope to have this feature soon.

To protect your business purchases, we recommend reviewing the merchant’s refund policy or checking if your specific card network (e.g., Visa or Mastercard) offers separate Chargeback rights for faulty goods.

As the iwoca Credit Card is for businesses and not for private individuals, it does not fall under Section 75 of the Consumer Credit Act 1974 and joint liability does not apply to your transactions.

Applying for an iwoca Credit Card will not affect your personal credit score and will not appear on your personal credit report. This is because we run a soft search on your personal credit file when you apply.

Like many business credit card providers, we ask for a personal guarantee when you apply for a credit card. If your business falls behind on repayments, it may have an impact on your personal credit score. Find out more about personal guarantees here.