Business loan calculator: what you could repay

Use our calculator to find out how much you can borrow and what your monthly repayments could be.

- From £1,000 to £1,000,000

- Repay early with no fees

- Get a decision in 24 hours

- From 1 day to 5 years

How the calculator works

Pick a loan amount and a term, and the calculator estimates your monthly repayment and total cost. It uses our 3.33% representative rate per 30 days to do the maths.

We charge interest on your outstanding balance, only for the days you're using the loan, not on the full amount for the whole term. So as you repay and your balance drops, the interest drops too. Your real rate is set once we've looked at your business, so your actual figure may be lower than the estimate here.

This loan calculator is only an example, your actual rate and repayment amount for your business loan will vary based on your circumstances. At least 51% of customers who take out a loan of £25,000 or less receive our Representative APR or a lower rate.

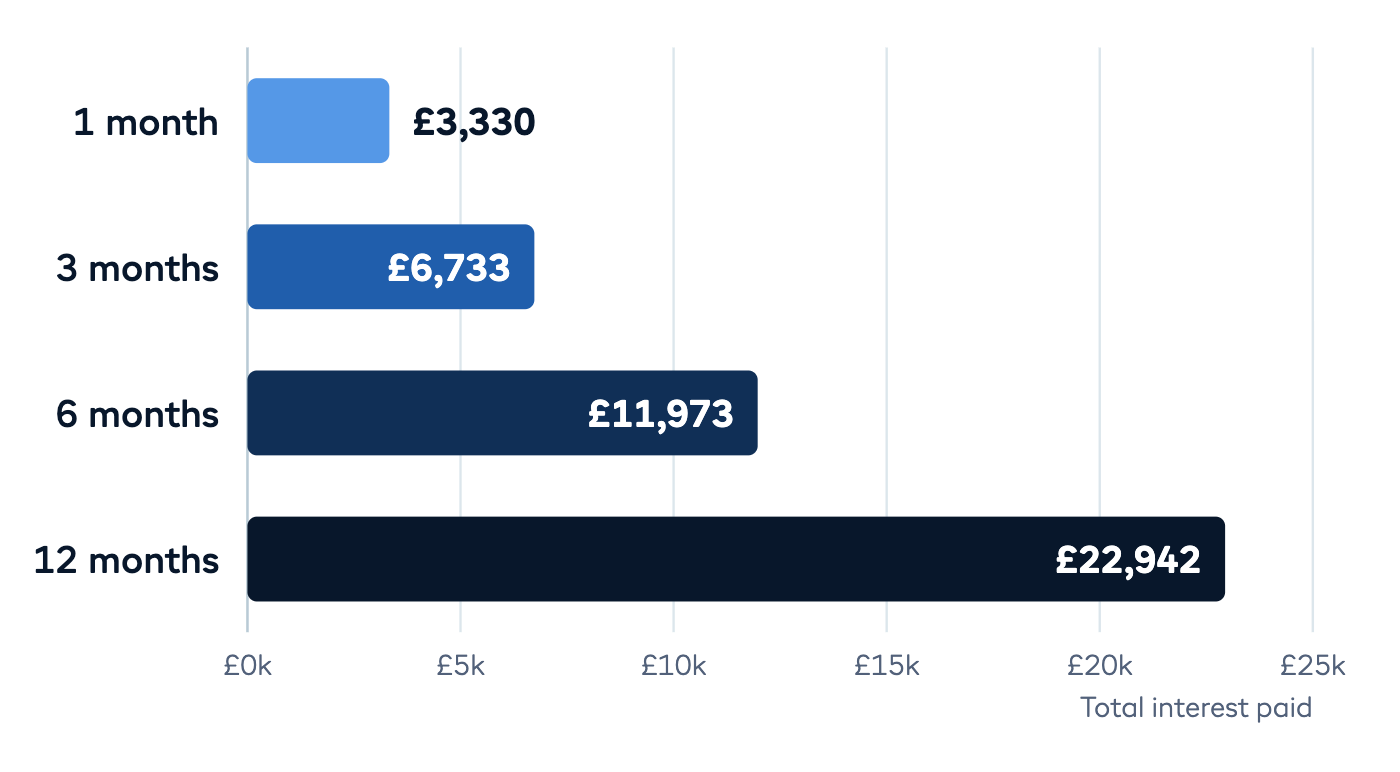

Repay early, pay less

Because interest is charged for the days you borrow, repaying early genuinely saves you money – and we never charge a fee for it.

Say you borrow £25,000 over twelve months but clear it in six. You'd only pay interest for those six months, not the full year. More than 20% of our customers repay ahead of schedule in their first six months.

So the term you pick sets your monthly repayment, but it never locks in the total cost. You can always pay less by paying sooner.

What amount should I enter?

If you're not sure how much you need, as a general rule you can borrow up to 20% of your annual turnover with iwoca, so maybe start there. Try a few amounts and terms to see how the monthly repayment and total cost change.

Your actual limit depends on your turnover and trading history. For the full detail on how much you can borrow, eligibility and newer businesses, see our business loan page.

Ready to apply?

.png)

What affects the rate you're offered

The calculator shows our representative rate, but your real rate is personalised. We base it on your business – things like your trading history, turnover and how you're performing. That's why the estimate here and your actual offer can differ.

Once you've got an offer, it stays open for 30 days. There's no pressure to decide straight away.

Business loan calculator FAQs

How is a business loan interest rate calculated?

We set your rate based on your business, then charge it on your outstanding balance for the days you're using the loan. As you repay, the balance falls and so does the interest. Our representative APR is 49%.

What loan amount should I put into the calculator?

Anything from £1,000 to £1 million. If you're not sure, around 20% of your annual turnover is a useful figure to start with. Our business loans page explains how much you can actually borrow and who's eligible.

How much does a business loan cost?

Rates start at 1.5% per 30 days, with a representative APR of 49%. There are no fees on 12-month loans; longer terms may include a fee. Use the calculator above for an estimate for your amount and term.

Can I repay early and save money?

Yes. Because you're only charged interest for the days you borrow, repaying early reduces what you pay – and there's never an early-repayment fee.

If I apply, do I have to take the funds?

No. An offer isn't a commitment. You can see your actual rate and amount, then decide. Your offer stays open for 30 days.

Loved by over 100,000 small businesses

(and big names) since 2012

%20(1).jpg)

Questions? We're here to help

Call us at 020 3778 0274 from Monday to Friday (9am - 6pm). We can take your business loan application over the phone, or answer your questions about applying online.